How Mortgage Lender can Save You Time, Stress, and Money.

Table of ContentsThe Basic Principles Of Mortgage Mortgage for DummiesWhat Does Mortgages Do?What Does Mortgages Near Me Do?

15-year loans were cheaper at 4. 06%. ARMs were even cheaper, with prices as low as 3. 13% readily available. Our rate tables are updated day-to-day as well as will certainly reveal you the most recent prices for your area. There are 4 core elements of a home mortgage repayment: the principal, interest, tax obligations, as well as insurance, jointly referred to as "PITI." There can be various other expenses consisted of in the repayment, as well.

If you were to get a $100,000 home, for example, and also borrow $90,000 from a lending institution to help spend for it, that would certainly be the principal you owe. The rate of interest, shared as a percentage price, is what the lending institution charges you to obtain that cash. In other words, the rate of interest is the yearly cost you pay for obtaining the principal.

The mortgage's promissory note is what in fact represents the car loan. One more essential point: While a home mortgage is secured by actual residential or commercial property (in various other words, your residence), other types of car loans, such as credit cards, are unsecured, says Jodi Hall, president of Nationwide Mortgage Bankers, Inc., in Melville, New York.

The Single Strategy To Use For Mortgage Lender

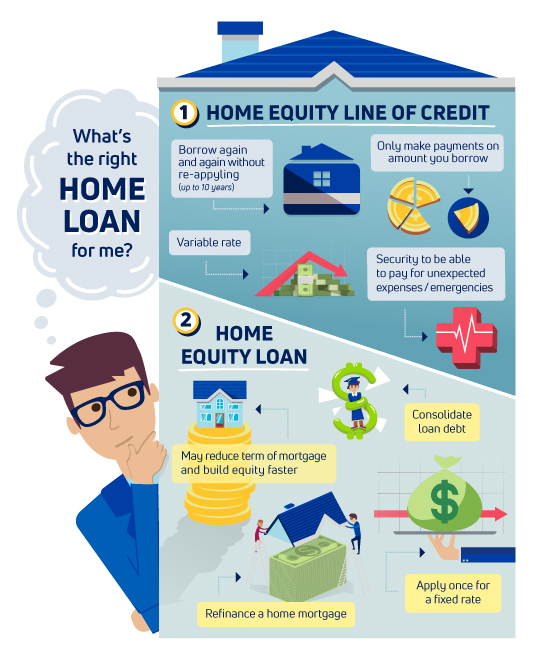

If the home were to be seized and also the loan provider sells the building, the proceeds of the sale would certainly initially approach paying off the initial home loan, due to the fact that it's in the senior lien setting. A 2nd home loan describes a lien in a junior position, such as a house equity line of credit report (HELOC) or home equity financing.

Strive to make all of your credit card, funding or various other financial debt payments on schedule, and check your credit history reports for any kind of errors before getting a home mortgage. If you identify inaccurate info (like wrong get in touch with information), conflict it with the credit rating reporting bureau asap to get it fixed.

As you evaluate your home loan choices, right here are some fundamental terms you may come across (and also below are other crucial terms to recognize). Amortization defines the procedure of settling a finance, such as a home mortgage, in installation repayments over a period of time. Part of each settlement goes towards the principal, or the quantity obtained, while the other portion goes towards passion (Buy a Home).

When a car loan fully amortizes, that suggests it's been repaid completely by the end of the amortization routine. APR, or interest rate, mirrors the expense of obtaining the cash for a home loan. A more comprehensive measure than the rates of interest alone, the APR includes the rates of interest, discount factors as well as other costs that include the finance.

The Single Strategy To Use For Team Quintez - Integrity Home Mortgage Corporation

The down repayment is the amount of a home's purchase rate a buyer pays upfront (Buy a Home). Purchasers normally take down a portion of the house's value as the down payment, after that obtain the rest in the form of a home mortgage. A bigger deposit can assist improve a borrower's opportunities of obtaining a lower rate of interest.

An escrow account holds the portion of a debtor's monthly home loan payment that covers house owners insurance premiums and also residential property taxes. Escrow accounts likewise hold the down payment the customer deposits in between the moment their deal has been accepted and also the closing. An escrow account for insurance coverage and also taxes is normally established up by the mortgage loan provider, that makes the insurance policy and tax repayments on the consumer's part.

The servicer collects your payments and, if you have an escrow account, ensures that your taxes and insurance are paid on time. The servicer also tips in with alleviation alternatives if you're having difficulty making repayments.

A home loan is most likely to be the biggest, longest-term car loan you'll ever before obtain to buy the most significant possession you'll ever before possess your home - mortgages. The even more you understand how a mortgage works, the much better furnished you need to be to pick the home mortgage that's right for you. A mortgage is a car loan you obtain from a loan provider to fund a house acquisition.

The Ultimate Guide To Mortgages

Here are some usual terms you'll need to recognize if you're getting a home mortgage: The promissory note, or "note" as it is extra frequently labeled, browse around this web-site details how you will settle the finance, with details consisting of: Your rate of interest Your total funding amount The term hop over to these guys of the loan (30 years or 15 years are common examples) When the loan is thought about late Your regular monthly principal and also interest settlement.

The home loan offers the loan provider the right to take possession of your residence and offer it if you do not make payments at the terms you agreed to on the note. An action of trust fund works like a mortgage as well as is safeguarded against your home. Many home mortgages are arrangements in between two parties you as well as the loan provider.

An act of trust fund gives the trustee the authority to take control of your home on behalf of the loan provider if you stop paying. These are expenditures billed by a lender to make or stem your lending. They normally the original source consist of source costs, discount points, fees connected to underwriting, processing, file preparation as well as funding of your finance.

While costs differ widely by the sort of mortgage you get as well as by area, they normally total 2% to 6% of the lending quantity. So on a $250,000 mortgage, your closing costs would amount to anywhere from $5,000 to $15,000. Called "home mortgage factors," this is money paid to your loan provider in exchange for a lower rates of interest.